Although employers must still meet minimal benefit levels that at least match what would be provided under the normal work comp system, the allure of the Oklahoma opt-out program is greater control over the process.

When I see what is happening in states across the nation, with new frictional costs associated with every attempt to "reform" programs, it's easy to understand that allure.

According to Workers’ Compensation Director James Mills, there are currently three insurers approved to write policies for the Oklahoma Option: OneBeacon Insurance Co., Safety National Casualty Corp. and Great American Security Insurance Co. All three were approved in April.

Whether more carriers offer packages will obviously depend upon market appetite for this new program, though Midlands Management representatives told WorkCompCentral that the company is working on the final stages of filing to become an approved carrier to offer its own Oklahoma Option policy.

Tom Hebson, vice president of development and government relations, business development, for Safety National, told WorkCompCentral that the company has also received five "submissions" to opt out, though none of those employers fit Safety National's employer profile. Hebson also said that there have been "well over" another 10 "inquiries" from much larger companies exploring their options.

|

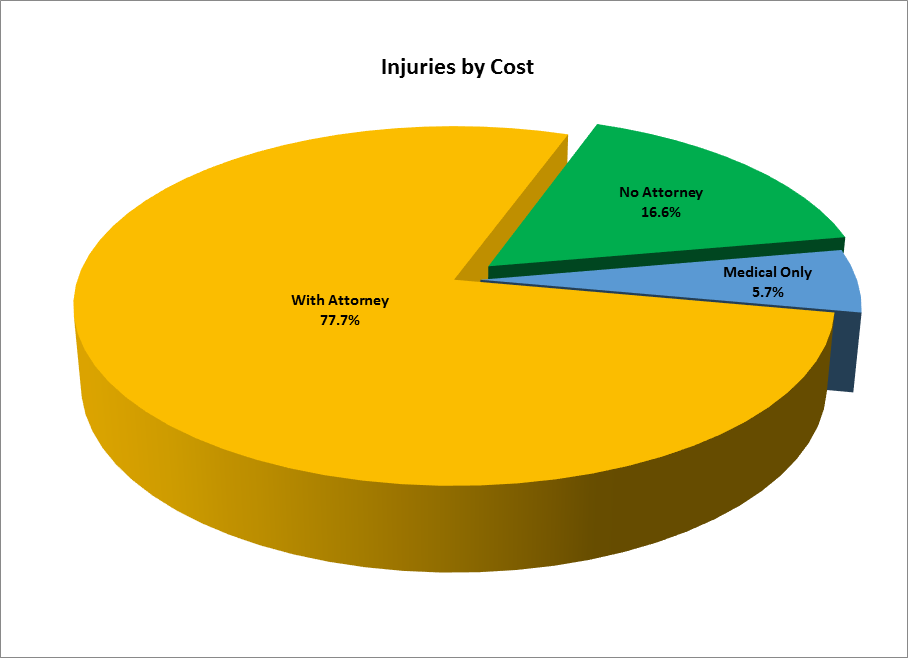

| In CA, 11% of cases comprise almost 78% of costs. |

What is happening in Oklahoma should be of high interest to the workers' compensation industry - escaping what sometimes seems to be ponderous regulation is very attractive to the folks that ultimately have to pay the cost of providing some work place protection - employers - and could spur a whole new cottage industry, particularly if other states follow Oklahoma's lead.

While Texas does not mandate employers subscribe to the workers' compensation system, most businesses do.

According to Rod Bordelon, who will be retiring as Texas Workers' Compensation Commissioner August 1, over 80% of the state's employees are covered by workers' compensation policies in the state.

Texas' reform in 2005, HB 7, greatly altered the landscape in that state. According to Bordelon, injury frequency and severity are down by big numbers.

Bordelon told the House Business and Industry Committee last April that injury rates are down 27% since 2004. Claims have fallen 22% since that same year. Requests for benefit review conferences, the initial step in dispute resolution, have also gone down, although statistics showed an increase in the number of disputed issues within benefit review conferences and contested case hearings in recent years.

According to Bordelon, 93% of all claims now get resolved without going through the dispute resolution process in Texas.

Workers’ compensation insurance rates fell 50% from 2003 to 2011, and the percentage of employers who don’t subscribe to Texas’ voluntary workers’ compensation system fell from 38% in 2004 to 33% in 2012, according to Bordelon.

The Texas experience from the past has reflected that when workers' compensation premiums are stable and at acceptable levels to business, more employers go with the system rather than alternative risk systems or completely "going bare."

In addition to allowing employers to engage an alternative risk system, when Oklahoma introduced it's option the state also introduced significant changes to it's traditional system.

If Oklahoma experiences a decrease in its workers' compensation costs, it will be interesting to see how many employers that are opting out now stay with those programs.

And with other states feeling tremendous pressure of reformation promises that aren't being realized, namely California, it may come to pass in a few years that the business lobby will seek similar options. There's no question when I go out in the field and talk to employers in California that there is huge disappointment with SB 863 and discontent overall with the state's work comp system.

California, representing over a quarter of the entire nation's workers' compensation market, would be a huge plum for carriers and brokers with an appetite for providing alternative risk coverage.

Certainly nothing will happen in California without a tremendous fight from all of the special, virtually protected, interests that comprise the industry, but the single best argument in favor of controlling California's cost of work injury protection is market competition - i.e. the ability to take one's business elsewhere.

And Texas has shown that good market competition puts pressure on a system to be competitive. Though some in Texas contend that system savings were put on the backs of injured workers (and anecdotal evidence does reflect that Texas injured workers now have a much harder time getting attorney representation to assist with disputes) the fact remains that subscription rates are up.

The more employers that subscribe, the more capital there is in the system, which brings costs down for everyone participating in the system, which puts pressure on alternative systems to keep costs down in order to compete for that premium dollar.

At the end of the day, all that really matters is whether employees have some reasonable protections in place in the event of an unfortunate work place accident, and that the risk of having to pay for those protections is spread out sufficiently so that no one single business is overly burdened.

It's a nearly impossible ideal to achieve. An Oklahoma report card in a few years will tell us whether that state has hit upon a reasonable and sustainable method of resolving the conflict between the social mission and the business mission of workers' compensation.

No comments:

Post a Comment